We're part of the Convasio Studio.

© 2026 Convasio Studios.

Find out more about Kenyan real estate using AI

Ask JuliaWe're part of the Convasio Studio.

© 2026 Convasio Studios.

Eastleigh money is driven by trade, trust, and pooled family capital with a long-term, generational focus. Westlands money, on the other hand, is structured around formal employment, banking systems, and debt-based investments. The real difference lies in how capital is built, shared, and risk is managed—not in culture or background

market

If you spend time observing Nairobi’s real estate growth, a quiet pattern emerges. New high-rise residential and mixed-use projects in Kilimani, Kileleshwa, South C, Ngong Road, and Upper Hill are increasingly associated with developers linked to Eastleigh, alongside Chinese developers.

This often triggers surface-level explanations around religion, ethnicity, or access to money. But those explanations miss the core issue. What we are really seeing is different philosophies of capital operating within the same city. Eastleigh money and Westlands money are not just sourced differently, they behave differently, especially under pressure.

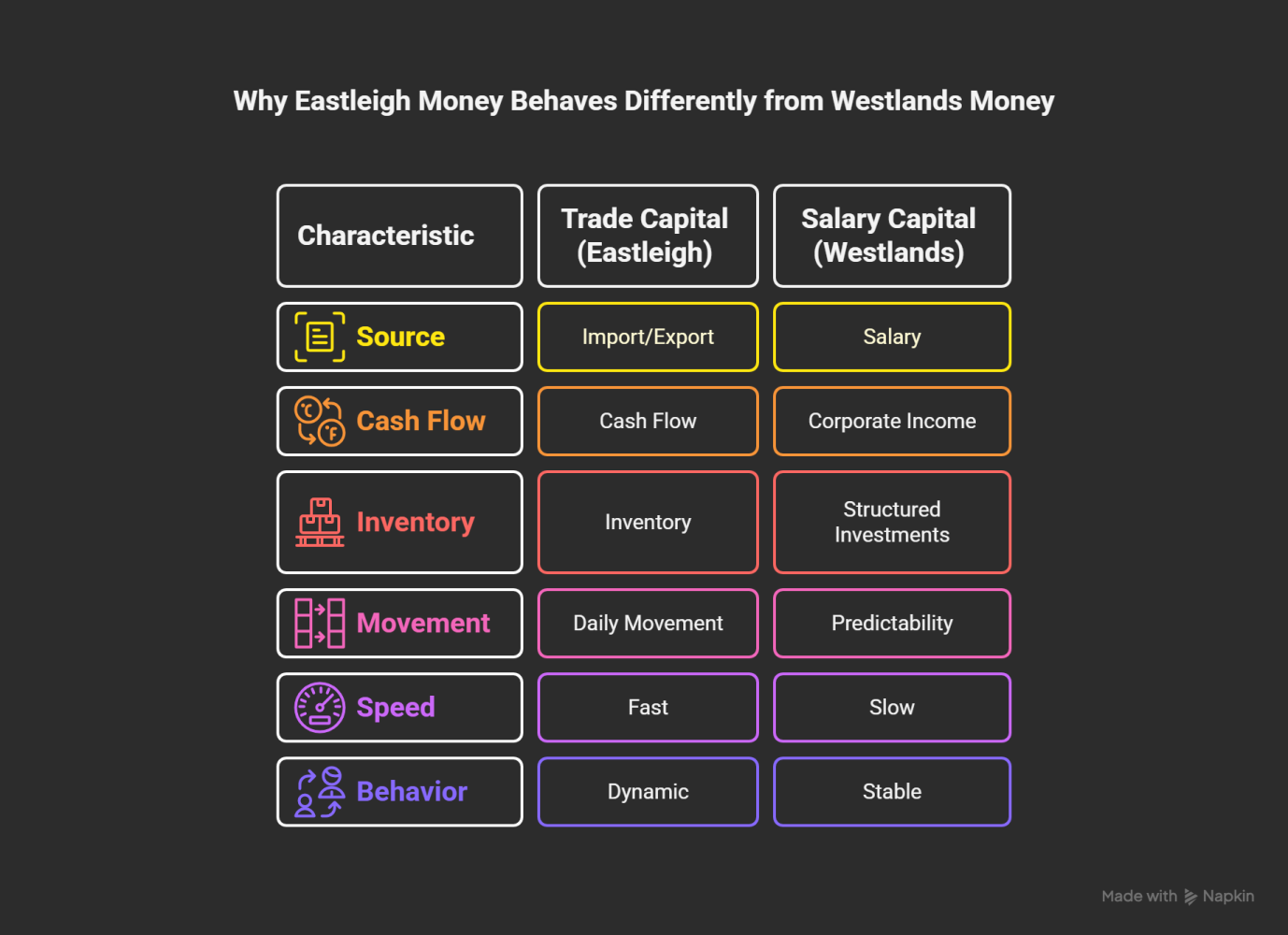

One of the biggest differences lies in where the money originates. Eastleigh money is largely trade-based, coming from import and export businesses, wholesale and distribution, manufacturing, logistics, and cash-heavy retail operations. This kind of capital moves daily, depends on inventory turnover, and survives on cash flow rather than projections. Westlands money is more often salary or corporate-derived. It comes from executive and professional income, formal employment, equity-linked investments, and bank-structured opportunities. It is predictable and well-modeled, but slower to move.

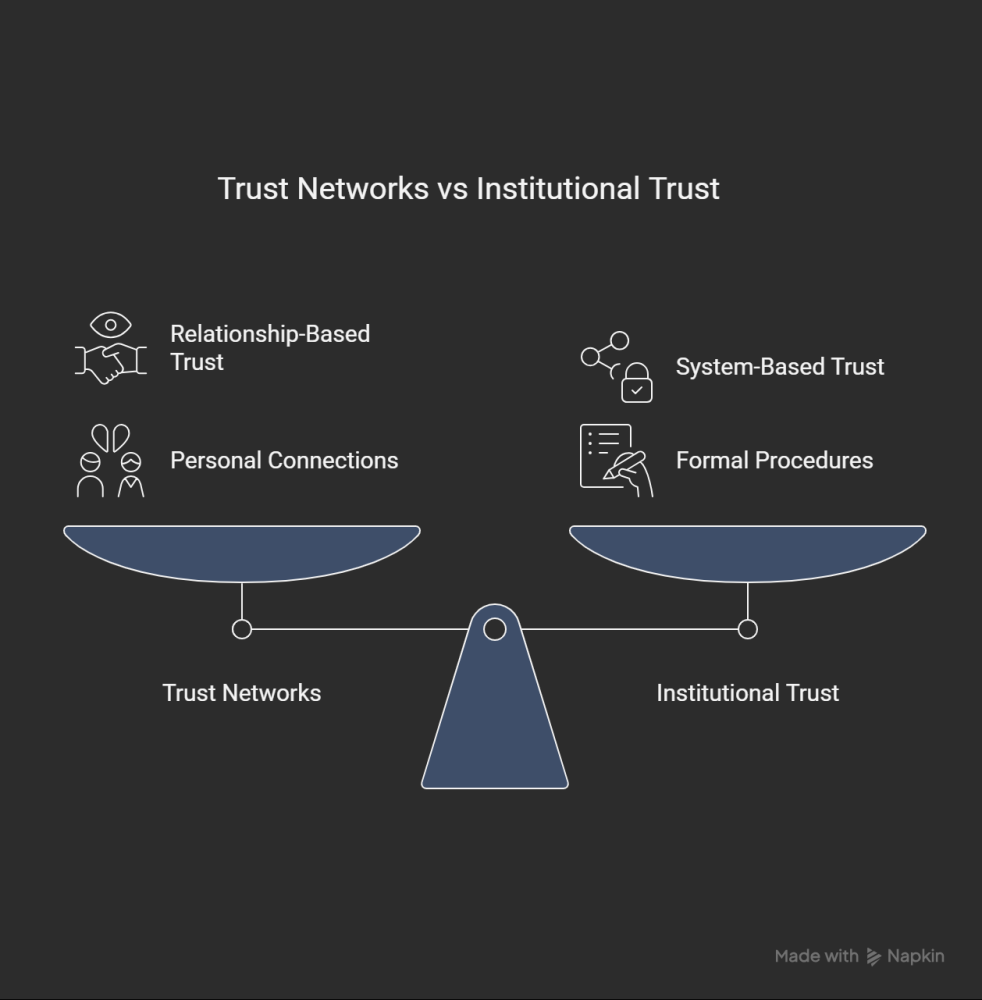

Eastleigh-linked investments typically rely on family partnerships, long-standing business relationships, reputation-based enforcement, and social accountability. Verbal commitments carry weight, and failure has real social consequences. Westlands investments tend to rely on banks, lawyers, contracts, compliance frameworks, and formal governance. This approach emphasizes documentation, legal enforcement, and risk transfer.

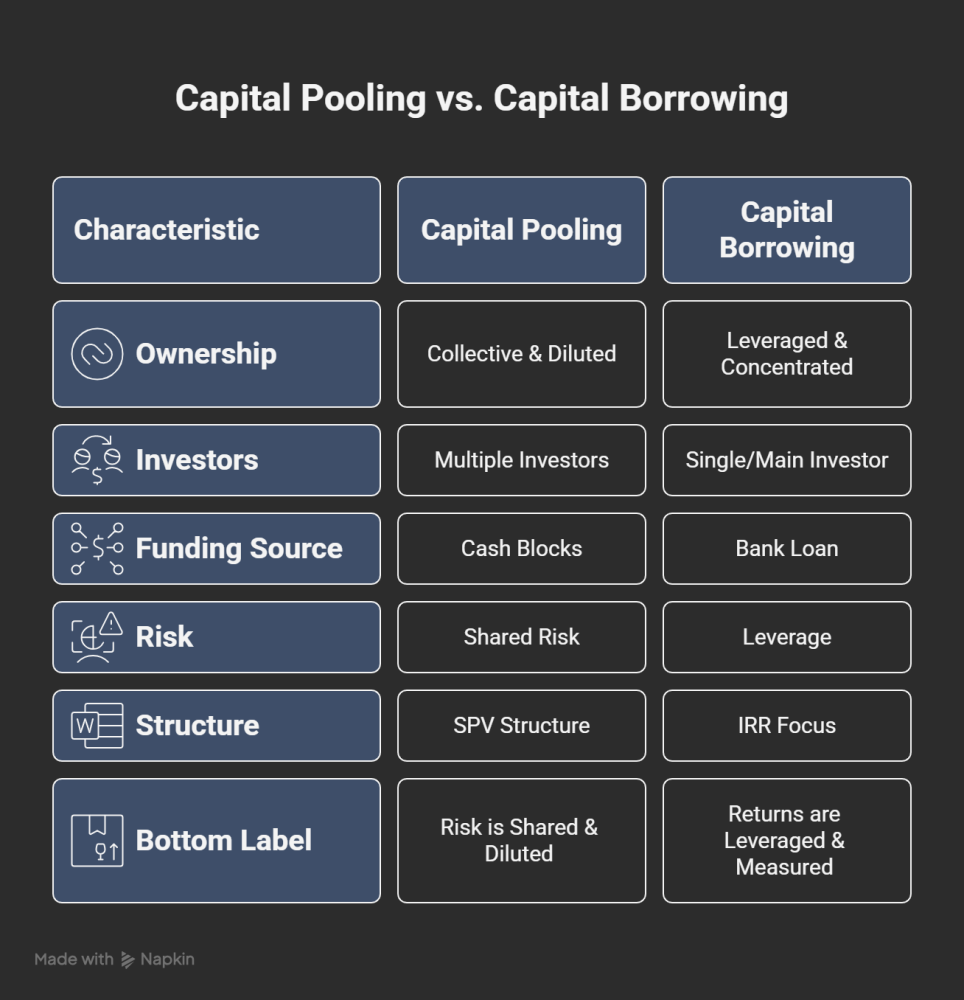

Eastleigh investors often assemble large projects through capital pooling. Multiple individuals contribute large blocks of cash, ownership is diluted, and risk is shared. Projects are commonly held through Special Purpose Vehicles (SPVs) entities created specifically to own and operate a project). Westlands investors typically favor capital borrowing. Equity is preserved, returns are enhanced through leverage, and performance is measured using tools like Internal Rate of Return (IRR), a metric estimating investment profitability.

Many Eastleigh-linked families operate with generational time horizons. Land was often acquired decades ago, developed slowly, and rarely sold. The objective is preservation and steady growth. Westlands capital is usually cycle-driven, operating on five to seven year horizons with defined exit strategies.

For Eastleigh capital, cash flow collapse is catastrophic, debt is dangerous, and price volatility is manageable. For Westlands capital, volatility can be hedged, debt is a tool, and illiquidity is acceptable if structured.

Religious frameworks are often cited, but they are not the primary driver. They reinforce behavior rather than create it. The real drivers are how capital is raised, how losses are absorbed, who bears reputational risk, and how long investors can wait.

Cities are not shaped by who has more money. They are shaped by how money behaves when conditions change. Eastleigh and Westlands are not competing neighborhoods. They are two financial philosophies quietly building the same city one deal at a time.